For those who believe that magazine covers are great contrarian indicators, this September Time magazine cover reflects enough pessimism to call the bottom of the US housing market.

----------------------------------------

From a letter sent to President Bush by Barney Frank, Nancy Pelosi, Maxine Waters and 73 other Congressional Democrats on June 28, 2004:

"We urge you to reconsider your Administration's criticisms of the housing-related government sponsored enterprises (the GSEs) and instead work with Congress to strengthen the mission and oversight of the GSEs. We write as members of the House of Representatives who continually press the GSEs to do more in affordable housing.

"Until recently, we have been disappointed that the Administration has not been more supportive of our efforts to press the GSEs to do more. We have been concerned that the Administration's legislative proposal regarding the GSEs would weaken affordable housing performance by the GSEs, by emphasizing only safety and soundness. While the GSEs' affordable housing mission is not in any way incompatible with their safety and soundness, an exclusive focus on safety and soundness is likely to come, in practice, at the expense of affordable housing.

"Our position is not based on institutional loyalty, but on concern for the GSE's affordable housing function. We appeal to you to agree to work on legislative proposals that foster sound oversight and vigorous affordable housing efforts instead of mounting assaults in the press. We also ask you to support our efforts to push the GSEs to do more affordable housing. Specifically, join us in advocating for more innovative loan products and programs for people who desire to buy manufactured housing, similar products to preserve as affordable and rehabilitate aging affordable housing, and more meaningful GSE affordable housing goals from HUD.

"In closing, we reiterate that an exclusive emphasis on safety and soundness, without an appropriate balance in focus on the affordable housing mission of the GSEs, is misplaced."

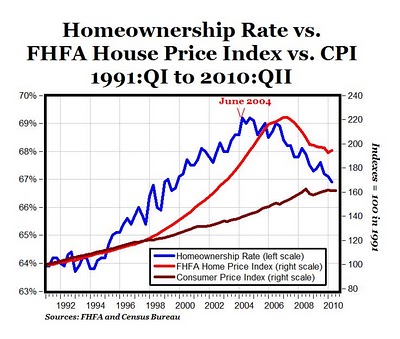

The Grouch: The above graph reflects the conditions of the housing market in 2004 when the letter was sent from Congress to then President Bush:

- Homeownership was at an all-time historical high of 69.2% in the second quarter of 2004, and had increased by more than 5% from 63.9% in the first quarter of 1991.

- Home prices had been inflating at a rate far greater than the general price level for almost a decade, as the unsustainable housing bubble was on its way to the 2007 peak in home prices. At the time the letter was written in 2004, home prices had appreciated by 85.4% since 1991, which was more than twice the 39.6% increase in the CPI over that period. Historically home prices appreciate in line with CPI.

- At the time homeownership was peaking and home prices were close to peaking, both at unsustainable levels, the politicians in 2004 were still pushing for the "ownership society" and all of the policies that eventually caused the global financial crisis, mortgage tsunami, and housing bubble: affordable housing through lower down payments, looser underwriting standards and higher leverage (Of course, when the financial crisis hit in 2007-2009 they all came down with a bad case of amnesia).

I couldn't agree more with these conclusions. In fact, I don't see how we can have any serious financial reform in this country until the link between housing and politicians is broken for good. Fannie and Freddie need to be broken up into a "good bank/bad bank," so the bad bank could be wound down and the good bank broken up into multiple pieces and privatized-- no more GSEs with private profits and public losses subject to political manipulation. But I don't think the politicians willingly give up this type of power. What do you think?

HT: Carpe Diem

I agree that GSEs need to be disbanded. I also agree that the emphasis on home ownership was overdone. Still all of this to a certain has been done since the early 1970s and some of it was necessary to pick up the pieces emanating from the S&L bust. The bottom line IMHO is that the Fed screwed up big time by pushing short rates to 1% in 2003. If they had kept rates at 3% and above we would have had a mild downturn and the housing market wouldn't have gone crazy.

ReplyDeleteI agree with you that the Fed was a contributor to the problem. However, I think the role of Fannie and Freddie has been deliberately downplayed and hidden. Their very existence retarded the development of a private mortgage securitization market that would have had more discipline on mortgage standards, and they were the enablers of these crazy securitizations of sub-prime and alt-a mortgages that were misrated by the rating agencies and marketed by the sharks on Wall Street.

ReplyDelete